Debt relief can be a way for people to ease their financial burden, but many borrowers don’t realize that sometimes forgiven debt can lead to tax consequences. Borrowing money isn’t income, but things can get interesting when a lender cancels or forgives some of a loan.

This is called cancellation of debt income (COD income). In some cases, the IRS may treat the amount forgiven by a lender as taxable income.

In this guide, we’ll cover what cancellation of debt income means, how it works, when it’s taxable, and important exceptions that might apply.

Cancellation of debt (COD), refers to when a lender forgives, cancels, or discharges all or part of a debt that a borrower owes.

Normally, when you borrow money, the amount received is not considered taxable income because you are expected to repay it. However, if you are no longer required to repay some or all of that debt, the forgiven amount may be treated as income.

A lot of people don’t know what to do with their money.

Suppose you have $10,000 in a credit-card account. They negotiate with the lender and settle on forgiving $4,000 of the debt.

Total debt: $10,000

Repaid to date: $6,000

Debt forgiven: $4,000

The $4,000 forgiven may be treated as cancellation of debt income.

The process usually follows a simple pattern:

Let’s say you borrowed $10,000 on a credit card. Over time, you managed to pay back $6,000, but you couldn’t keep up with the rest. The credit card company agrees to settle and cancels the remaining balance.

That $4,000 could show up as income on your tax return for the year the debt was cancelled — even though you never physically received that money as cash.

Not all debt situations are identical. Several types of loans and obligations can potentially create COD income.

Credit card companies sometimes negotiate settlements with borrowers who have financial problems.

If a portion of the balance is forgiven, the cancelled amount might be taxable.

Mortgage Debt

Sometimes lenders forgive some of a mortgage after a foreclosure, short sale or loan modification.

Special tax rules may apply in certain circumstances

Personal loan balances that are forgiven may become taxable.

Some student loan forgiveness programs may qualify for special exclusions under federal rules.

If a lender “forgives” a remaining balance on a vehicle loan, there may be tax consequences.

Businesses that receive debt forgiveness may also face cancellation-of-debt income rules.

As a general rule, yes. The IRS considers forgiven debt to be taxable income, and lenders are required to report it to the IRS when the forgiven amount is $600 or more.

However, “generally taxable” doesn’t mean “always taxable.” There are specific, well-defined exceptions where forgiven debt does not count as income — and these exceptions matter a lot, because they can save you from an unexpected tax bill.

The short version:

Because the rules depend heavily on individual circumstances, this is one of those tax situations where getting it right matters. A tax professional or IRS-approved software can help you confirm which category you fall into.

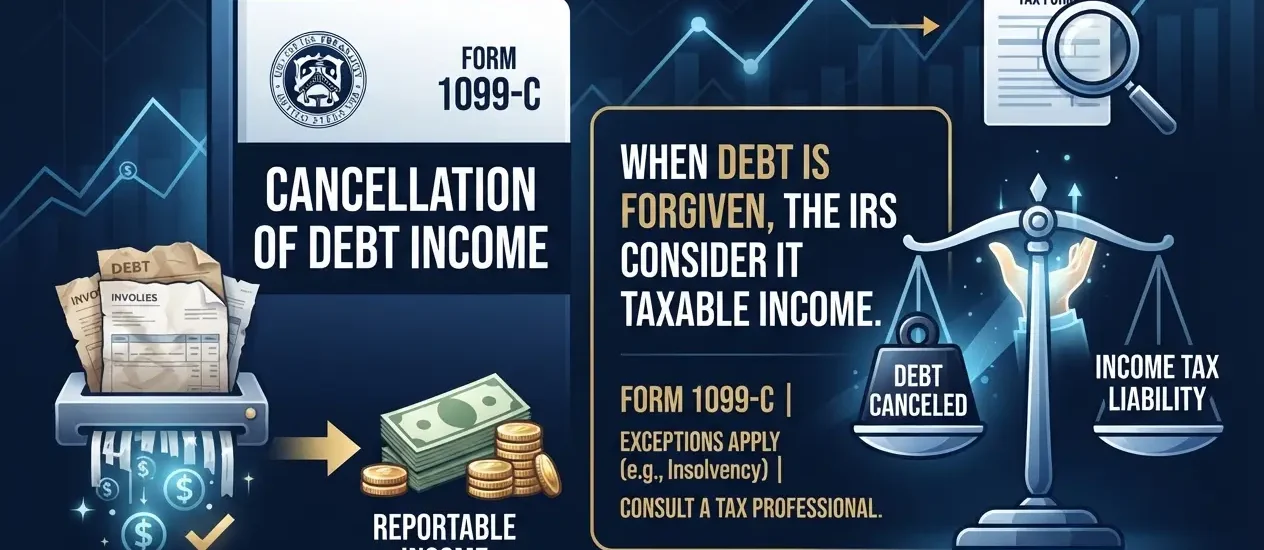

Form 1099-C, “Cancellation of Debt,” is the tax form lenders use to report forgiven debt to both you and the IRS.

If a lender cancels $600 or more of your debt, they’re generally required to send you a 1099-C and file a copy with the IRS. This creates a paper trail so the IRS can match the forgiven amount against your tax return.

Lenders typically issue Form 1099-C by January 31 for debt cancelled in the previous calendar year. You might receive it from a credit card issuer, a mortgage lender, an auto lender, or even a debt collection agency that purchased and later forgave your debt.

The form will show the amount of debt cancelled in Box 2. You’ll generally need to report this amount as “other income” on your tax return, unless one of the exceptions below applies — in which case you’d typically use Form 982 to claim the exclusion.

This is the section that matters most if you’ve received a 1099-C and are worried about a tax bill. Several major exceptions can reduce or completely eliminate your taxable COD income.

1. Bankruptcy

Debt discharged through a Title 11 bankruptcy proceeding is generally excluded from taxable income.

2. Insolvency

If your total debts were greater than the total value of your assets immediately before the cancellation, you may qualify for the insolvency exclusion. You can exclude cancelled debt up to the amount by which you were insolvent.

Simple example:

If $8,000 of debt was cancelled, none of it would be taxable, because it’s fully covered by your insolvency amount. If $12,000 was cancelled, only $4,000 (the amount exceeding your insolvency) would potentially be taxable.

3. Certain Student Loan Forgiveness Programs

Some student loan discharges — such as those for death, permanent disability, or certain public service and income-driven repayment forgiveness programs — may be excluded from taxable income under current law. Rules here have shifted in recent years, so it’s worth confirming the current status for your specific program.

4. Qualified Principal Residence Indebtedness

If your primary home mortgage debt was forgiven (through foreclosure, short sale, or loan modification), you may qualify for an exclusion under rules specifically designed for principal residence debt, subject to dollar limits and eligibility requirements.

Example 1: Credit Card Settlement

Sarah owes $8,000 on her credit card.

The lender agrees to settle the debt for $5,000.

The forgiven $3,000 could potentially be treated as COD income.

Example 2: Mortgage Debt

John experiences financial hardship and negotiates with his lender.

His remaining mortgage balance is reduced by $20,000.

Depending on applicable rules and exclusions, some or all of the forgiven amount may have tax consequences.

Example 3: Student Loan Forgiveness

Emily qualifies for a public service loan forgiveness program.

Depending on current tax regulations, the forgiven balance may qualify for exclusion.

Like many financial situations, debt cancellation has advantages and disadvantages.

Q:Is cancellation of debt income always taxable?

No. Certain situations such as bankruptcy, insolvency, and some student loan forgiveness programs may qualify for exclusions.

Q: What happens if I receive Form 1099-C?

You should review the information carefully and determine whether any exceptions apply before filing your tax return.

Q: Does cancelled debt affect credit scores?

Debt settlements and loan forgiveness situations can potentially affect credit scores depending on circumstances.

Q:Can student loans create cancellation of debt income?

Some student loan forgiveness programs can create tax consequences, while others may qualify for exclusions.

This article is for general informational purposes and shouldn’t be considered tax advice. Tax situations vary based on individual circumstances, so consult a licensed tax professional or CPA before filing if you’ve received a 1099-C.